Banking on resilience: building capacities through financial services inclusion

Introduction

Financial inclusion is often seen as critical to development and would make sense even without climate change (World Bank, 2016). It may also help vulnerable groups in developing countries become more resilient to climate extremes and global warming. The poorest and most marginalised in society are most affected by climate-related shocks because they often live in hazardous places and typically have fewer resources and access to social safety nets (Wilkinson and Peters, 2015).

‘Resilience’ has many meanings, but the climate change and disasters literature commonly draws on definitions from socio-ecological systems theory, which refers to the properties of a system that allow it to deal with shocks and stresses, to persist and to continue to function ‘well’ (in the sense of providing stability, predictable rules, security and other benefits to its members). Resilience is derived from various capacities that are interlinked: absorptive, anticipatory and adaptive capacities. A social system with these capacities is less likely to be undermined by shocks and stresses, so well-being can be ensured and human development can continue to progress in locations exposed to climate extremes and disasters (Bahadur et al., 2015).

Saving and borrowing can strengthen some of these capacities, helping people to plan ahead, adapt to changes, and absorb shocks when they happen, but these services are not always accessible to the most vulnerable in society. Financial inclusion is therefore a key policy area for building resilience and should focus on increasing access to saving and money transaction services for vulnerable groups as well as the provision of credit and insurance at an affordable cost (Zwendu, 2014).

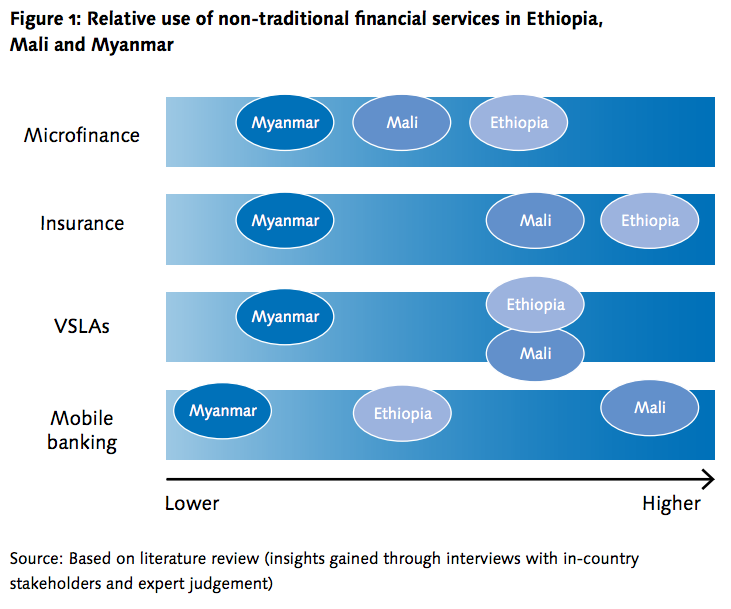

This BRACED policy brief*looks at experiences in Mali, Ethiopia and Myanmar in helping to build resilience to climate extremes and disasters through increased financial inclusion.

*download the full text via links provided under Further Resources. The key policy messages and recommendations are provided below.

Key Policy Messages

-

FINANCIAL SERVICES INCLUSION helps build climate resilience and nontraditional financial services are better able to reach the most vulnerable, but action is needed on the demand and the supply side.

-

A MORE TRANSPARENT REGULATORY FRAMEWORK for these services can help promote inclusion and growth in the sector (and so competition and flexibility), alongside protection for users and improved physical access for the most vulnerable.

-

SUPPORT TO SERVICE providers is needed to build capacity, financial literacy and trust of vulnerable and disadvantaged groups in the banking system.

Recommendations

Governments and international development agencies can take a variety of actions to support the development of financial services in a way that promotes climate-resilient development. A comprehensive set of measures is required, on both the supply and the demand side of the financial system.

One key measure relates to strengthening the enabling environment for improvements in financial inclusion and depth. Governments will need to improve regulatory and legal frameworks to make them more transparent and predictable, reducing costs and simplifying rules to enter the market. On the demand side, greater protection for users is needed, as well as improved physical access for the most vulnerable. All of this will improve competition and flexibility in the market and trust in the banking system. In addition, international development agencies and donors can offer financial, legal and technical support to financial service providers in order to help them expand and scale up the offer of services at an affordable cost, as well as provide products that promote a risk management ethic indecision-making. All this will need to be focussed on building the climate resilience of the most vulnerable.

The formal private sector offers a unique competitiveness in the provision of financial services, and this should be exploited. For example, it can develop new financial and communications technology services, such mobile banking applications tailored to specific user needs that could help to expand mobile/ telecoms network coverage.

Governments and donors need to collaborate with non-governmental organisations and service providers to build the capacity, financial literacy and trust of vulnerable and disadvantaged groups in the banking system. This includes providing training on disaster risk reduction, preparedness and business skills linked to the delivery of financial services, so that these products can be used effectively by vulnerable groups to build their resilience. Training initiatives could usefully build on the experiences of existing programmes, such as the SfC programme carried out by CARE, Plan International and World Vision.

This research was written by Anna Haworth, Camille Frandon-Martinez, Virginie Fayolle (Acclimatise Ltd.), and Emily Wilkinson (ODI)

BRACED (Building Resilience and Adaptation to Climate Extremes and Disasters)aims to build the resilience of more than 5 million vulnerable people against climate extremes and disasters. It does so through a three year, UK Government funded programme, which supports 108 organisations, working in 15 consortiums, across 13 countries in East Africa, the Sahel and Southeast Asia. Uniquely, BRACED also has a Knowledge Manager consortium.

Website: www.braced.org

Twitter: @bebraced

Facebook: www.facebook.com/bracedforclimatechange

Suggested Citation

Haworth, A., Frandon-Martinez, C., Fayolle, V., and Wilkinson, E. (2016) Banking on resilience: building capacities through financial services inclusion. BRACED Policy Brief. London: Overseas Development Institute

(0) Comments

There is no content