The New Frontier of Adaptive Finance for Disaster Recovery

Introduction: The Need For Adaptive Post-Disaster Financing

According to Munich RE, a German reinsurance firm, disasters in 2016 caused $175 billion dollars of damage. Only 30% of that damage is covered by insurance, and governments, non-profits and NGOs struggle to make up the difference during recovery and reconstruction. This means that there is a $122 billion opportunity for the financial sector to assist, if they can develop products sufficient to meet post-disaster financing needs. The case for why the financial sector should focus on financing post-disaster reconstruction hinges on the fact that financial systems rely on healthy markets. After a disaster, damaged and uninsured companies and businesses are unable to sell their products and services. This in turn presents a huge risk to the financial industry that backs their operations, and/or the operations of other companies that rely on such businesses in their supply chain or distribution networks. Likewise, uninsured households must rebuild, and this process requires products and services that are customized to their needs as disaster survivors. However, financing post-disaster reconstruction is not easy and happens in an environment that is chaotic and changing continuously. To meet the needs of damaged markets and survivors in post-disaster contexts, the financial sector will have to adapt its methods of developing and delivering products and services.

How to Apply Adaptive Financing to Support Long-term, Sustainable Disaster Reconstruction

In many post-disaster circumstances, the financial products available to consumers and businesses are unable to meet their needs, because the customers’ circumstances have changed so much after the disaster. If individuals and companies are forced to pick from standard loan products and other financing mechanisms, they can easily find themselves adopting a greater burden in that the size of the loan, terms and tenor may not be realistic given their new situation. Thus, the decision to desperately take out an ill-fitting loan can not only increase the vulnerability of a customer, it can also also create additional risk for the financial institution. In this report (download available here and from the right-hand column) we explore how the private sector can be creative and create flexible products that can adapt to the needs of post disaster survivors, enabling them to reconstruct and alleviating the challenges posed by risks to capital investments in times of uncertainty. What is adaptive financing?Adaptive financing is a type of financial product that is flexible enough to adapt to the needs of specific locations in the wake of disasters. Changing conditions demand flexibility. Some product-development processes create fixed products. For example, a mortgage is a product that a client can buy. However, if a client wants to change the fixed terms of their contract, they generally have to refinance. In contrast, adaptive financing offers flexible products that can adapt to changes in customer situations. This adaptability depends on flexible underlying processes that allow for finance providers to make ongoing adjustments to products in response to changing client needs. This requires a redesigned product-development process and a new conception that a financial product is a service instead of a commodity.

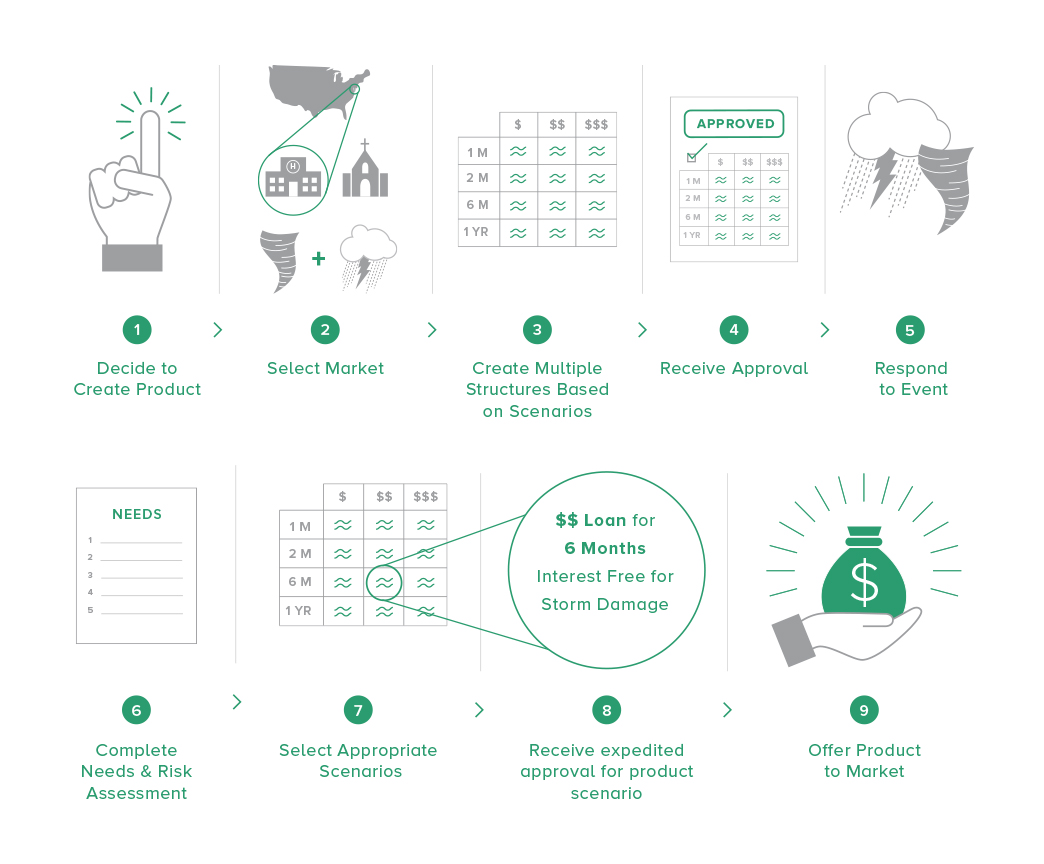

One example of an adaptive financing instrument is displayed in figure 1. In this framework, the private insurers have a pre-determined suite of insurance options, linked to a variety of disaster scenarios. This way, when disasters occur, the insurer is prepared to select the appropriate scenario and provide a suitable product to the market, as opposed to relying upon business-as-usual financial tools for addressing an un-usual situation.

Report Methodology

To understand how the private sector could create such flexible and adaptive financial products, we facilitated a workshop at Yale University with experts from the humanitarian-response and private-finance worlds, ranging from The World Bank’s Global Facility for Disaster Reconstruction to Citibank. Conclusions and recommendations included in the resultant report (presented here) were based on workshop outcomes, background interviews, and additional research.

Barriers to Adaptive Financing

We identified the following major challenges associated with designing adaptive products for post-disaster relief:

- The complexity of post-disaster scenarios

- Damage to markets and disruption of supply chains

- Challenges associated with balancing risk and return in uncertain environments

- Slow and cumbersome product-development processes

- The difficulty of coordinating the deployment of public and private capital

- The lack of trust between financiers, agencies, and recipients after disasters

These challenges and others keep adaptive financing mechanisms from being sponsored by product development teams at financial institutions that are seeking to maximize value and minimize risk.

Enabling Factors and Solutions

However, through actions like development of partnerships, use of creative design and research techniques, and adequate consideration of planning, innovation can help private financiers reduce the challenges of post-disaster financing. Additionally, many of these actions can help accelerate the product development timeline so that provide timely, effective relief to people in need.

A full list of recommendations and suggested methods for enabling more adaptive financing products and processes is available in the report (download available from the right-hand column).

Outcomes and Impacts

What were the key findings of this project and their associated impact?

If banks can help restart markets, not only can they they help prevent their clients from facing default, they can also enjoy additional benefits like strengthened customer/supplier loyalty, enhanced brand reputation, and valuable experience that can push the capabilities of the organization, spurring new internal innovation.

Lessons Learnt

From this investigation, we identified the following challenges and proposed the following solutions. These are the key takeaways for those working in private capital or disaster recovery and response seeking to become more nimble and climate sensitive in their financial product development processes. See the full text for much more detail.

| Challenges of Post-Disaster Financing | Example Recommended Adaptive Approaches |

|---|---|

| Financing after Disasters Requires New Models of Product Development |

|

| The Case for Private Investment in Disaster Reconstruction Is Underdeveloped |

|

| Disasters Disrupt Supply Chains and Complicate Recovery Logistics |

|

| Larger Markets Can Be Damaged by Disasters |

|

| Slow and Cumbersome Financial-ProductDevelopment Processes Lead to a Mismatch in Timing Between Need and Available Financing |

|

| Complexity Can Pose Obstacles during Disaster Recovery |

|

| Exploitative Behavior Can Affect Community Trust |

|

| Lack of Preparation for a Disaster Increases the Magnitude of Impacts |

|

This is a framework that is intended to kick-start the conversation about what role the private sector can play in disaster reconstruction finance. However, more work needs to be done at the organization level to pilot adaptive products that are viable and contribute to a community’s needs. We suspect that many additional challenges will arise during such processes that will also be worth sharing with the field.

This report, authored by Laura Hammett, Yale MEM 2017, and Katy Mixter, Yale MEM and MBA 2017, was supported by Yale Center for Business and the Environment. It received funding from the Class of 1980 Fund at the Yale School of Forestry and Environmental Studies.

Suggested Citation

Hammett, L. and Mixter, K. (2017) Adaptive Finance to Support Post-Disaster Recovery. Yale Center for Business and the Environment: New Haven, U.S.A.

(0) Comments

There is no content